Will Home Prices Drop in 2026? Here's What the Data Says Right Now

Every week somebody lands in my DMs with a version of the same question: "Jason, is the crash finally coming?"

And honestly, I get it. We're sitting here in June 2026 with mortgage rates still stubbornly above 6%, a median existing home price that just hit $429,300 an all-time high for the month of May, and a Fed that just voted unanimously to hold rates steady again. If you're a buyer trying to make the math work, the frustration is real and completely valid. Bankrate

But frustration and market reality aren't the same thing. So let me give you what I always try to give you on this blog: the data as it actually stands, not the narrative someone is trying to sell you.

What Are Home Prices Actually Doing in June 2026?

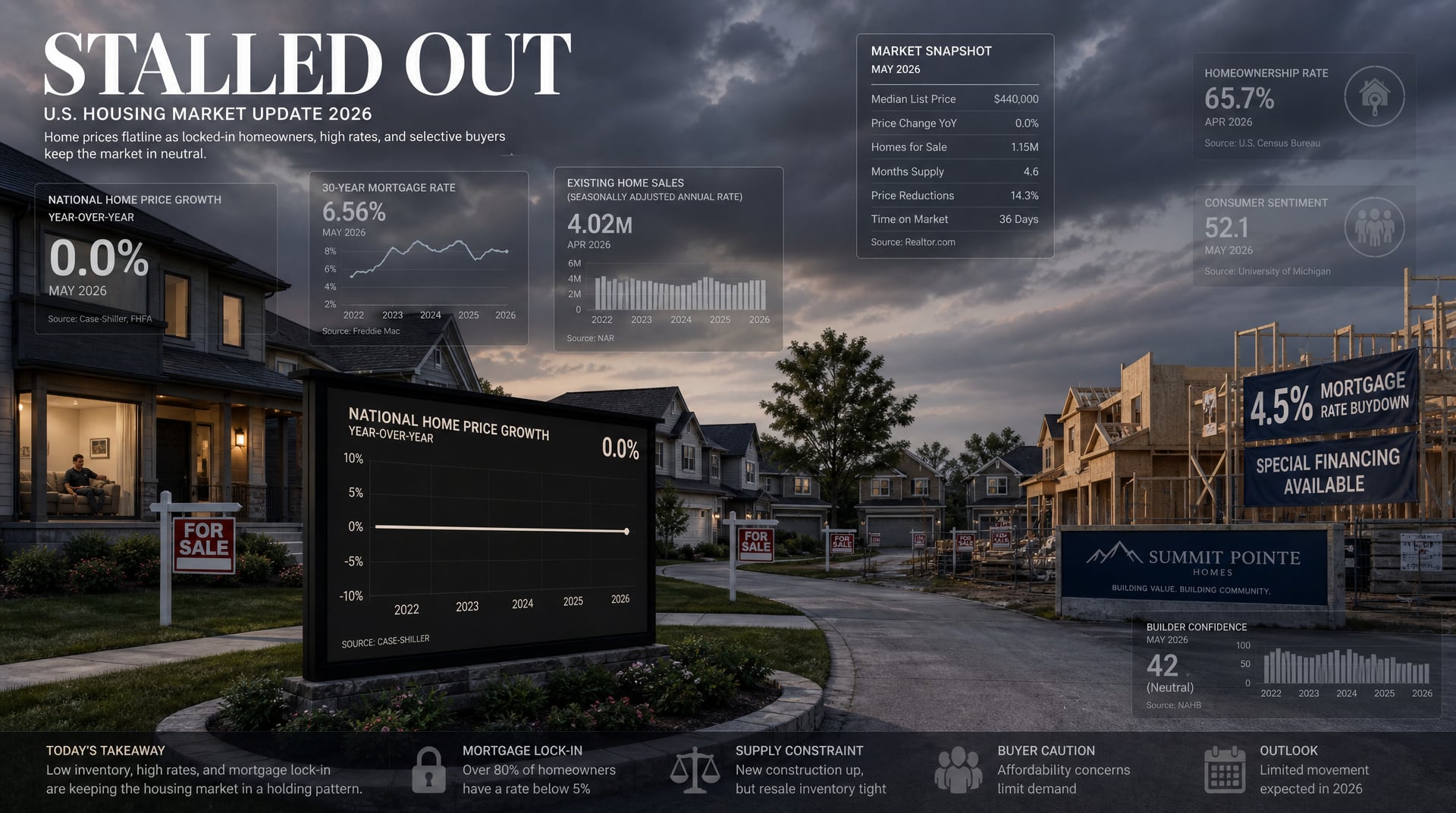

The headline number you need to know: J.P. Morgan Global Research projects U.S. home prices to stall at exactly 0% growth nationally in 2026. That forecast, which came out earlier this year from John Sim, head of Securitized Products Research at J.P. Morgan, has held up through the spring selling season and nothing in the current data suggests it needs to be revised upward. J.P. Morgan

The S&P Cotality Case-Shiller index released in late May showed national home prices grew just 0.7% in the past year — the weakest showing since 2011, when prices fell 3.9%. Let that sink in for a second. We are at the slowest pace of appreciation in fifteen years. The boom is unambiguously over. But notice what it did not say: prices did not crash. Bankrate

Zero to flat growth. That's your 2026 housing market in a sentence.

Why Are Home Prices Refusing to Fall Despite Brutal Affordability?

This is the question that keeps pundits up at night, and the answer is actually pretty elegant once you understand the mechanics.

The lock-in effect is still doing the heavy lifting. Tens of millions of American homeowners are sitting on pandemic-era mortgages in the 2–3% range. If you have a 3% mortgage, you probably don't need a research note to explain why you're hesitant to move and for first-time buyers, that individual hesitation shows up as a painful lack of listings. People are not selling. And when people don't sell, supply doesn't flood the market, which means prices don't have anywhere to fall to. TheStreet

Existing home sales rose just 0.2% in April over March, landing at a 4.02 million annual pace, while unsold inventory rose to 1.47 million units about 4.4 months of supply. More options than a year ago, yes. But nowhere near the volume that would trigger a meaningful price correction at the national level. U.S. Bank

On top of the lock-in dynamic, household balance sheets remain generally healthy. U.S. homeowners are sitting on roughly $35 trillion in equity. Forced selling — the mechanism that actually triggers price crashes is nearly nonexistent. Without distressed inventory hitting the market, there's simply no catalyst for the kind of price spiral the crash crowd has been predicting for three years running.

What's Really Driving Mortgage Rates in June 2026?

Here's where the macro story gets genuinely complicated, and it's something I think a lot of people aren't fully connecting to their home-buying calculus right now.

Inflation spiked in May to 4.2% the highest level since 2023. Oil prices have spiked amid the conflict in Iran, pushing inflation up and lifting mortgage rates from their 2026 low of 6.09%. Bankrate

As of last week, the average 30-year mortgage rate in Bankrate's weekly survey was 6.48%, as markets digest the war in Iran and rising oil prices. Housing economists expect rates to stay above 6% for the rest of the year. Bankrate

That's the environment we're operating in. The Fed voted unanimously to hold its benchmark rate steady on June 17th, and the decision was described as "unanimous and unambiguous" by Chairman Kevin Warsh. Rising inflation has been the main driver of higher mortgage rates ,the consumer price index has pushed well above the Fed's 2% target. Bankrate

So if you're waiting for mortgage rates to fall significantly before you buy, here's the uncomfortable reality: in a May 2026 U.S. News survey, nearly two-thirds of homebuyers (62%) were waiting for mortgage rates to fall before buying a home , the same amount (62%) who put off buying in 2025 for the same reason, and they didn't fall. Waiting has a track record right now, and it's not a good one. U.S. News & World Report

Are There Markets Where Home Prices ARE Dropping Right Now?

Yes and this is critical nuance that a national headline number buries entirely.

The 0% figure is a national average that masks dramatic regional divergence. Prices are falling quickest on the West Coast and in the Sunbelt. Texas home prices are down 2.4% from a year ago, and Florida home prices are down 5.1%, according to Zillow. These are markets where builders rushed to add supply during the pandemic relocation boom, and now that overbuilding is sitting on the market, pressuring values. Fortune

More than half of the 20 major U.S. housing markets recorded year-over-year price declines in March, reflecting a broadening and deepening housing slowdown. Bankrate

So when someone asks me, "Are home prices dropping?" the honest answer is: nationally, barely. But locally, in the Sun Belt and along the West Coast, meaningfully. If you've been priced out of a Florida or Texas market and have flexibility in your timeline, the data suggests you now have negotiating power that simply didn't exist two years ago.

What Are Homebuilders Doing to Move Inventory Right Now?

This is the part of the story I find most tactically useful for anyone actively trying to buy , because this is where real money is being left on the table.

New single-family home sales ran at a 622,000 annual pace in April 2026, with 489,000 homes for sale and 9.4 months of supply, which gives builders more reason to use pricing flexibility or financing incentives to keep sales moving. Builder confidence remains subdued, with the NAHB/Wells Fargo Housing Market Index at 37 in May 2026. U.S. Bank

When builder confidence is at 37 and they're sitting on 9.4 months of supply, they are motivated. Deeply motivated. And the tool they keep reaching for is the mortgage rate buydown.

Most homebuilders already offer potential buyers mortgage rate buydowns of 100 to as much as 200 basis points below the prevailing mortgage rate. At current market rates hovering around 6.5%, that means a builder buydown can realistically land your effective rate in the 4.5–5.5% range. On a $400,000 loan, that difference in monthly payment is enormous , we're talking several hundred dollars a month that stays in your pocket. J.P. Morgan

The builders aren't lowering their prices. They're buying down your rate instead, and achieving the same practical effect on your monthly cash flow. It's a strategy built for this exact environment, and I think a lot of buyers are walking past it because they're too focused on waiting for the headline price to drop.

Should You Buy a Home Right Now or Keep Waiting?

I'll give you the same honest framework I'd give someone sitting across from me at a coffee shop.

If your plan is to wait for a dramatic national price crash, the structure of this market makes that scenario unlikely in the near term. The lock-in effect is real. Household equity is deep. Forced selling is minimal. The conditions that produce a 2008-style correction overleveraged homeowners, loose lending standards, cascading defaults are simply not present.

U.S. homeowners are sitting on roughly $35 trillion in equity. Lending standards are tighter than they were in 2008. Supply is still tight in most markets. That's not the setup for a crash.

What is present: a new construction market where builders are highly motivated and actively subsidizing your entry cost through rate buydowns, and a handful of Sun Belt and West Coast markets where price corrections are already underway.

The buyers who will win in this environment aren't the ones who perfectly time the bottom. They're the ones who identify the specific pockets where inventory is high, builders are aggressive, and the deal math actually pencils out with current incentives , then act with conviction.

The Bottom Line on Home Prices — June 2026 Edition

Here's where we stand: national home prices are flat, sitting near 0% annual growth. Mortgage rates are holding around 6.5% with inflation running hot and the Fed unwilling to cut. Existing home sales are barely moving. Builders are aggressively buying down rates to clear supply that's sitting at the highest levels since 2010 in some markets. And regionally, Sun Belt and West Coast markets are seeing real price softening while the Northeast and Midwest hold relatively firm.

No crash. No boom. A plateau with sharp regional variations and a window of builder incentives that won't stay open forever.

I'll have updated numbers for you again next week. In the meantime — drop your market in the comments and tell me what you're seeing on the ground. That local data is always the most honest signal.